General information

As at 31 December 2019, Alior Bank served 4.0 million of consumers. The increase of customer base in 2019 resulted from Alior Bank’s organic growth and acquisition of SKOK “Jaworzno”.

The Bank has operated a project of behavioural segmentation of retail customers, which enables us to precisely address products and services to the appropriate audience. Behavioural segmentation is useful both for the construction of the product offering, and support of the sales network. In 2019, the Bank continued its strategic segmentation of customers. Strategic segmentation has been implemented in the entire outlet sales network. The bankers and advisers were equipped with comprehensive knowledge on how to recognise customer needs and how to talk about them so that to sell products best suited to their needs. By the middle of the year we have implemented behavioural segmentation also in selected areas of remote channels.

In September 2019, work has begun on updating our behavioural segmentation. In 2020, a new approach will be presented which handles this topic on broader terms to better respond to customer profiles and address their needs.

In addition to behavioural segmentation, the Bank has distinguished the following operating segments among its retail customers:

The above-mentioned segmentation is reflected in the structure of the sales network by specialisation of sales units: universal branches, premium branches and Private Banking, respectively.

Distribution channels

At the end of 2019, the Bank held 820 outlets (197 traditional branches, 7 Private Banking branches, 8 Corporate Centres, and 608 partner outlets). The Bank’s products were also offered within the network of 10 Mortgage Centres, 9 cash centres and a network of about 5000 intermediaries.

In December 2019, the Bank’s first branch created in a new format was presented. It is distinguished by its innovative design and new technologies used. The role of the branch is above all to provide comfort and privacy to customers and working comfort to bankers. Materials used are eco-friendly and products come from local suppliers.

Alior Bank has also used distribution channels based on its state-of-the-art IT platform comprising: online banking, mobile banking and call centres as well as DRONN technology. The Bank uses the Internet, including through online banking, to enable its customers to make contracts for: personal accounts, currency accounts, savings accounts, term deposits, debit cards and brokerage accounts. These channels also accept applications for credit products: cash advances, credit cards, overdraft facilities and mortgage loans. Through the Internet, the Bank also has offered hire-purchase loans handled online and enables its customers to use Currency Exchange Bureau services.

Traditional branches of Alior Bank are distributed throughout Poland, especially in cities and towns with more than 50,000 residents, offering full range of its products and services. Partner outletsare located in smaller towns and in selected locations in the main cities of Poland, offering a broadrange of savings & credit services and products for retail and business customers.

The bank collaborates with its partner outlets based on outsourcing agency contracts. Under such agency contracts, agents provide only agency services on behalf of the Bank for the distribution of the Bank’s products. These services are provided from the premises owned or rented by the agents approved by the Bank.

As mentioned above, the Bank’s products are offered through a network of financial intermediaries, such as Expander, Open Finance, Sales Group, Dom Kredytowy Notus, Fines, and others, which mainly offer cash advances, consolidation loans and mortgage loans, as well as hire-purchase loans.

One of the key strategic initiatives in 2019 completed by the Bank in collaboration with PZU was to open a new distribution channel for cash advances – the Cash platform. This platform is owned by PZU and is based on the technology provided by the Bancovo.pl service. It will be made available to employees of selected, big establishments. It applies full online process which the customers handle themselves, and the income information provided by them is verified and certified directly by their establishment. An important feature of this process is that repayment is made by deducting instalments from employee’s wages and salaries directly by the employer. The first to get access to the platform where PZU Group employees, and more companies follow suit in the future.

Sales support in all distribution channels is provided by operational and analytical Customer Relationship Management (CRM) systems.

Loan products

Cash loans

Cash loans

The main product from Alior Bank’s consumer credit offering is the cash loan. It may be spent for any purpose or for the repayment of financial debt (consolidation loan). Cash loans are available in all distribution channels of the Bank. In 2019, Alior Bank continued its strategy for cash loan sales in two streams. One involves attracting a new group of customers and cross-selling to the existing base, including a large group of customers attracted in the process of selling hire-purchase products. In order to attract new customers, the Bank has introduced in Q1 2019 an “Atypical Advance” offering, whose price depends on the amount of liability. In Q2, a broadly communicated TV campaign has started for the “Advance with Microcosts” product which offers an attractive price to customers. The cost of such advance is no more than 6 zloty per month per each 1000 zloty of net advance/loan. The offering is available in outlets, by remote channels, as well as through online banking. The Bank’s offering also features a special “Online Loan” offering for new customers who, by applying through a dedicated online application form, enjoy preferential interest terms and no commission. The contract could be signed by customers themselves through online banking or remotely, with the assistance of a call banker.

In delivering its plans for cross-selling to its existing customers, the Bank was preparing, on a cyclical basis, offerings for the existing advance customers using preferential pricing and simplified loan origination process, both through outlet channels and through online and mobile banking. In addition, a system for the acquisition and cross-selling to Consumer Finance customers has been implemented. What is called “onboarding” are measures to build brand awareness in the initial months of cooperation with the Bank to activate customers in digital channels and to persuade them to buy products and special offerings, not only the cash loan, but also other products addressed to consumers.

The onboarding of customer with instalment products figures into another area of the Bank’s activity – implementation of a new approach to the distribution of the advance – linking it with other areas of banking addressed to consumers. Under that approach, the bank rewards active customers and encourages the existing and new customers to being active in daily banking. To deliver this approach, in Q4 2019 a “Cosmic Loan” (Pożyczka Kosmiczna) was prepared, to be broadly communicated on TV and in other media. Attractive advance terms – 0% interest rate – was conditional on the activity of customers using the Konto Jakże Osobiste account and their debit cards. This action supported both the purpose of cross-selling and up-selling to the existing customers and to build a primary relationship with the Bank.

In addition, in Q4 2019 the Bank, tapping the opportunities opened up by PSD2 Directive, allowed customers from other banks to apply for Alior Bank’s credit products without the need to provide income certificates. This is a facility provided by the Account Information Service (AIS). This solution is available in selected sales outlets and in the Contact Centre. By the end of Q1 2020, this facility is scheduled to be available throughout the entire sales network, also in processes (including online processes).

In the last quarter of 2019, Alior Bank started working on adjusting its business strategy and internal processes to the September CJEU judgement on early repayment of consumer loans.

Credit cards

As part of its credit card offering for retail customers, the Bank continued in 2019 the promotion of the following credit cards: “Mastercard OK!” and “TU i TAM”. The main benefit has remained moneyback: for the OK! card the domestic moneyback, operated in selected commercial outlets, and for the “TU i TAM” cards it is accounted for non-PLN transactions (including online transactions and those effected abroad). For the most affluent customers from the Private Banking segment, the offering still encompasses the prestigious World Elite Card, coupled with a concierge services package, i.e. the assistance of a specialised call centre, insurance and Priority Pass – opportunity to use airport lounge services.

Addressing the expectations of customers who, when travelling abroad, are often looking for the best form of payment, analyse currency exchange rates, not infrequently fearing hidden costs, the Bank has launched a promotion under which transactions with the “TU i TAM” Mastercard credit cards have been translated since June 2019 according to the NBP mid-rate without any extra charges and commissions from the Bank.

In addition to very favourable currency translation terms, the Mastercard “TU i TAM” card also provides access to discounts and priceless attractions offered under the Priceless Specials loyalty programme. What’s important, this promotion covers both new holders of the “TU i TAM” card as well as those who have held this type of product for a longer time, and in June it has become available free of charge to all customers, including through our online banking system, in addition to standard acquisition methods in outlets or through the call centre.

In the last quarter of 2019, in collaboration with Innergo (authorised representative of Apple in Poland), the Bank has prepared a promotional action by which new holders of the Mastercard OK! credit card can receive an extra discount to purchase Apple equipment when paying with their credit cards.

Overdraft facilities

Overdraft facility is the ability to borrow against a debit in the account. Debt can be incurred

multiple times up to the authorised overdraft limit, and each payment to the account reduces or clears the debt. The Bank offers overdraft facilities for PLN 500 and up to PLN 200,000 without any additional security or guarantee.

In 2019, there was a consistently growing interest in overdraft facility through electronic and mobile banking under our simplified online process. The process is made available to a selected group of customers taking into account optimum offering of x-sell as part of CRM activities.

Mortgage loans

Mortgage loans in Alior Bank are provided mainly for residential purposes related to the purchase of real property. These loans can also finance the finishing, refurbishment or adaptation of property, purchase of a plot of land and house construction. In addition, it is possible to get refund of expenditures incurred during the last 2 years for residential purposes. The amounts from these loans can be used for any purpose unrelated to business activity or to consolidate other liabilities.

Mortgage loans are characterised by long-term exposure (up to 30 years) and maximum LTV at 90%.

They are available against commission or, optionally, against life insurance.

In 2019, the Bank continued its prior policy in the mortgage loan segment which were sold through two primary distribution channels, i.e., branches and Mortgage Centres dedicated to the processing of applications from intermediaries. In 2019, the Bank offered mainly PLN-denominated loans for residential purposes, which are a dominant item of the mortgage loan portfolio. This offering was complemented with loans indexed to the GBP, USD, EUR for residential purposes, available to those who earn their income in foreign currencies.

In the second half of 2019, the Bank took measures to increase its share of mortgage loan sales in the largest, dominant markets. To achieve this, an attractive offering was launched, available to customers who buy their homes in seven biggest cities, i.e., Warsaw, Krakow, Wroclaw, Poznan, Szczecin, Gdansk, or Lodz. To deliver this policy, strengthening of the branch sales network has been planned for these cities. The year-on-year sales growth was 20%.

Deposit products

Term deposits

Consumers depositing their PLN funds are offered by the Bank with term deposits for new funds and standard term deposits with fixed interest rates and a broad range of available maturities. The deposits on offer also include term deposits in foreign currencies: EUR, USD, GBP and CHF. These term deposits can be revolving or non-revolving. In addition, customers interested in depositing larger amounts can take the opportunity of negotiable term deposits, whereby both the maturity and interest rate are set individually.

Savings accounts

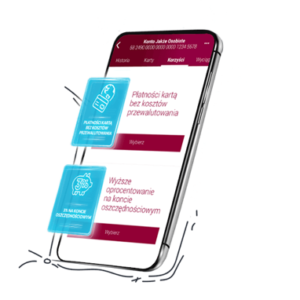

The Bank offers to its retail customers zloty-denominated savings accounts which encourage them to save while keeping flexible access to their funds. The main acquisition product is the 2018-introduced Konto Mocno Oszczędnościowe account, and the Konto Mega Oszczędnościowe account launched in December 2019. Its main benefit is preferential treatment of new funds up to PLN 100,000 for three months, by which higher interest accrues to customers who provide regular cash inflows to Alior Bank’s personal account. In addition, the holders of the Konto Mega Oszczędnościowe account have the option of flexible saving using free, unlimited online transfers to their personal account held at Alior Bank. In addition, the Bank offers higher interest on the savings account to customers who opt for the Konto Jakże Osobiste account and choose this feature as one of the benefits. Moreover, the Bank offers savings accounts addressed exclusively to new customers of the Bank and to customers who have successfully applied for the parental benefit (Family 500+ Application). They can enjoy preferential, fixed interest rate.

Savings accounts

The Bank offers to its retail customers zloty-denominated savings accounts which encourage them to save while keeping flexible access to their funds. The main acquisition product is the 2018-introduced Konto Mocno Oszczędnościowe account, and the Konto Mega Oszczędnościowe account launched in December 2019. Its main benefit is preferential treatment of new funds up to PLN 100,000 for three months, by which higher interest accrues to customers who provide regular cash inflows to Alior Bank’s personal account. In addition, the holders of the Konto Mega Oszczędnościowe account have the option of flexible saving using free, unlimited online transfers to their personal account held at Alior Bank. In addition, the Bank offers higher interest on the savings account to customers who opt for the Konto Jakże Osobiste account and choose this feature as one of the benefits. Moreover, the Bank offers savings accounts addressed exclusively to new customers of the Bank and to customers who have successfully applied for the parental benefit (Family 500+ Application). They can enjoy preferential, fixed interest rate.

Personal accounts

Personal accounts

In 2019, the Bank was developing its personal account offering by adding new functionalities to the existing products.

The flagship account in our product range is Konto Jakże Osobiste, for which the Bank has been distinguished with EFMA Distribution and Marketing Innovation Awards for the most innovative personal account.

Under the Konto Jakże Osobiste, the customer is able to adapt the offering in online banking or mobile app to his or her needs, by selecting from among ten advantages. Frequent visitors will enjoy a new advantage to the Konto Jakże Osobiste, introduced in June 2019. The new functionality allows for card payments without extra currency conversion costs.

The Mastercard Bezcenne Chwile loyalty programme, initially available as one of the advantages of the Konto Jakże Osobiste account, has been made available in the first half of the year to all customers in the online banking system, and thereafter in the mobile app.

The offering of personal accounts is complemented by the Konto Elitarne account dedicated to the Private Banking segment, the Konto Internetowe (Online Account), the Podstawowy Rachunek Płatniczy (Primary Payment Account) and Currency Accounts kept in four primary currencies: USD, EUR, CHF, GBP. Holders of currency accounts can also use the multi-currency service which enables them to link their currency accounts kept in the USD, EUR, GBP to their debit card accompanying the Konto Jakże Osobiste or Konto Elitarne accounts.

Transactional services

Alior Bank offers a broad range of transactional services, including: incoming and outgoing cash payments, cash payments to accounts kept at the bank and at other banks, instant transfers and cashless transactions using cards. In delivering its “Digital Disruptor” strategy, the Bank has implemented in its mobile app innovative mobile payment methods through BLIK, Android Pay and Apple Pay, and since December it has also provided customers with the functionality of smart watch payments (Fitbit Pay and Garmin Pay). Throughout 2019, the Bank has launched multiple campaigns targeted at increasing deal volumes with debit cards, offering certain benefits, either financial or as points in the MasterCard Bezcenne Chwile Programme, rewarding customers for transactions made with debit cards. All these measures support the Bank in meeting its overarching goal in the daily banking area, i.e., building lasting customer relationships.

Currency exchange transactions

Currency exchange transactions

Currency exchange deals are available at the Bank’s branches, through online banking (PLN, EUR, USD, GBP, CHF), as part of currency conversion related to international transfers and card transactions abroad, as well as through special, dedicated dealing platforms (Autodealing, Kantor Walutowy (Currency Exchange Bureau) and at the Treasury Department). The Bank has made available to its customers foreign-currency transactions for the following currencies: PLN, EUR, USD, CHF, GBP, CAD, NOK, RUB, DKK, CZK, SEK, AUD, RON, HUF, TRY, BGN, ZAR, MXN and JPY.

Holders of the Konto Jakże Osobiste account are provided by the Bank with the additional option to use the multicurrency service which enables them to link their currency accounts kept in the USD, EUR, GBP to their debit card accompanying their Konto Jakże Osobiste account, and, as part of benefits of the Konto Jakże Osobiste account, a service of card payments without extra costs of currency conversion.

Bancassurance products

In 2019, voluntary life insurance has been a major addition to the offering of banking products. Like in the prior years, the main role was still played by borrower’s life insurance (called PPI) offered on advances and mortgage loans. Standalone products offered (depending on the product) in the online channel, through the call centre, or through the branch network remained an important element.

Under its insurance offering, in 2019 the Bank continued its activities to support sales growth and development of life insurance related to advances and mortgage loans.

As part of its standalone offering, the Bank offered in 2019 accident coverage, cancer coverage, motor insurance, residential and travel insurance. Towards the end of 2019 changes were made to the online banking platform which facilitated the availability of selected PZU and Link4 products, which so far had been available on the Bank’s website only.

In 2019, the Bank also offered group insurance being an extra benefit accompanying banking products. These also included assistance and travel insurance as part of the Konto Jakże Osobiste account, travel insurance added to credit and debit cards World Elite, as well as group and assistance insurance for hire-purchase loans. In addition, the product range has been complemented in 2019 with travel insurance offered on the Kantor Walutowy (Currency Exchange Bureau) platform.

The Bank is still focused on offering insurance under what is called an individual model, whereby it stands as insurance intermediary and receives compensation for that. The group model, under which the Bank stands as the policyholder, is used for free products for the customer as supplementation of the parameters to improve the parameters of the respective banking product.

Structured products and investment insurance

Under its First Programme of Issuance of Banking Securities, Alior Bank S.A. issued 20 series of securities with a combined nominal value of PLN 686 million. These papers were addressed in public offering to consumers and Private Banking customers with an appropriate investment profile, and to corporate customers. The issues of banking securities were characterised by 100-percent guarantee of the principal amount on the maturity date, and for four series also by guaranteed coupon to be paid to customers on the issuance closing date. The main part of interest depends on the movement of a market index which was usually chosen as part of the stocks or investment fund baskets. In 2019, 34 issues took place, of which the best one closed with 22.06% result. In November 2019, the Bank has originated subscription as part of public offering of 18-month structured bond with guaranteed principal amount on maturity. In addition, the Bank continued its offering of structured certificates for selected Private Banking customers with limited guarantee on the principal amount, and conditional early redemption – “autocall”. Twelve issues of such kind were carried out in 2019 for a total nominal value of PLN 117 million. The certificates were floated on the Warsaw Stock Exchange.

In August 2019, the Management Board of the Bank decided to open up the Second Programme of Issuance of Banking Securities of Alior Bank S.A. The maximum debt of the Bank from all issued and active Banking Securities may not exceed PLN 5,000,000,000 at any time during the operation of the Programme.

New products and services

In 2019, important new products and services for the personal customer segment offered by Alior Bank Capital Group included:

- CASH loan, provided through a dedicated platform to employees of chosen companies, where monthly instalments can be repaid directly from the employee’s (the borrower’s) remuneration,

- credit process with creditworthiness assessment based on solutions resulting from the PSD2; as part of the process, customers use AIS and provide the Bank with an access to their account history, which serves as the basis for determining their creditworthiness,

- promotional implementation of transparent rules for conversion of transactions executed in a currency other than PLN with the use of Mastercard TU i TAM credit card, where the Bank waived its commission for currency conversion,

- dedicated Travel Insurance offered as part of our Exchange Office,

- possibility to buy some stand-alone insurance in online banking.

Retail segment areas

Consumer Finance

Under its retail segment, the Bank has offered Consumer Finance products.

In 2019, we focused in the Consumer Finance area on maintaining the position of a leader in the market for hire-purchase loans by maintaining stable collaboration with the current partners, acquisition of new counterparties and by supporting out sales with seasonal campaigns to promote instalment loan sales. Under our “Digital Disruptor” strategy, we continued our projects related to the delivery of our key initiatives, as well as activities to intensify sales in the eco area.

For many months we have been offering eco-instalments which customers can use to finance their thermal insulation projects, replacement of obsolete heat sources, and installation of a photovoltaic system. We have joined consultations with the National Fund for Environmental Protection and Water Management to develop a friendly process to enable customers to finance their projects with the hire-purchase loan and facilitating the award of grants under the “Clean Air” governmental programme.

To improve the attractiveness of its hire-purchase loan offering, the Bank has implemented Extra Services Packages through its online channel to increase the comfort of loan repayment, enhance the security of the customer’s finances, and providing support in the event of unforeseen circumstances. Customer trust and security are our highest priority, therefore the number of customers covered by the BIK alerting service as part of the hire-purchase loan has increased. Our customers do not have to fear that someone would abuse their personal details and attempt to take out a loan using their name.

We have cut by half the times of processing and labour intensity of integration with online shops on the part of the Bank by implementing a quicker way to integrate online hire purchase deals with eCommerce entities based on REST API.

With a view to increasing the comfort of the hire-purchase loan offering, such loans are now accompanied by offering to the customer an agreement providing access to the Bank’s electronic channels. Through access to “electronic banking”, among other things, our customers can now apply online for other products offered by the Bank, e.g. opening an account, which surely strengthens the customer relationship. Such agreements assist customers in current management of loan repayment. Customers can more easily monitor the repayment of loan instalments, check the current schedule and repayment history. Such solution was also made available to foreign nationals holding a stay permit in Poland longer than for visitor stay.

Private Banking

Private Banking

The Private Banking programme is addressed to the wealthiest individuals who entrust the Bank with assets in excess of PLN 1 million. Customers are served by seven specialised Private Banking branches in: Katowice, Poznan, Krakow, Gdansk and Wroclaw, and two branches in Warsaw.

At the end of December 2019, the Private Banking line held slightly more than 6,000 customers who are offered a broad range of investment and credit products adapted to their needs.

The flagship product dedicated to this segment is Konto Elitarne account kept free of charge for Customers holding more than PLN 1 million worth of assets. Customers enjoy a number of benefits, such as individual assistance from a Private Banking banker, confidentiality of account balances, or prestigious debit card MasterCard World Elite, offered at no additional cost, with a rich package of extra services.

Holders of Konto Elitarne account are also targeted with promotional, cultural and sporting actions, such as special theatre shows, or golf tournaments held by PGA Poland. An important event was also a competition held in collaboration with MasterCard, with its main prize being travel to alpine ski World Cup races in Kitzbühel.

Brokerage activity

The Bank has operated brokerage activities through Alior Bank Brokerage House – a separate organisational unit. Brokerage services are offered through the Bank’s outlets and using remote distribution channels: Brokerage House’s Contact Centre, Alior Bank’s online banking system, Alior Giełda, a mobile app, and Alior Trader 2, a dealing platform.

At the end of 2019, the Brokerage House kept 76,200 brokerage accounts, 53,500 deposit accounts, and 6,600 Alior Trader accounts. The combined value of assets on investment accounts is PLN 8.06 billion. Total cash on the above-mentioned accounts was PLN 242.5 million. Compared to the prior year, the share of stock-exchange instructions executed through the Alior Giełda mobile app doubled to 27%. In 2019, 24% of transactions executed on the Alior Trader account were instructed through the mobile app.

In 2019, Alior Bank’s Brokerage House won, for the second year in a row, the Puls Biznesu ranking of the best Brokerage Houses. The first half of 2019 saw the completion of migration of Alior Bank’s customers, including the Brokerage House, to the new online banking system which provides for fully remote purchase of products and use of investment services. In April, the Brokerage House has also made available a new investment service – inwestycje.aliorbank.pl – for those who want to proactively invest their savings. In December, customers of the Brokerage House have been offered an opportunity to join a loyalty programme for PKN Orlen shareholders.

In accordance with new requirements, in 2019 the Brokerage House has implemented the designation of operation types on securities as per ISO 15022/200222 standards, and adapted its systems to security trading rounded to four decimal places.

The Alior Bank Brokerage House’s services also include the offering of units of Polish and foreign investment funds. As at 31 December 2019, Alior Bank collaborated with 13 Polish and foreign investment fund companies and intermediated in the purchase of units at PLN 1.5 billion within open-ended funds. For non-public closed-end investment funds, in 2019 the Brokerage House only conducted post-sales service. Total assets accumulated in investment funds through Alior Bank were PLN 2.27 billion at the end of December 2019.

As of 31 December 2019, Alior Bank’s Brokerage House stopped providing the Market Maker services.

Collaboration in attracting retail customers

T-Mobile Usługi Bankowe

T-Mobile Usługi Bankowe

In 2019, T-Mobile Usługi Bankowe (TMobile Banking Services) consistently pursued the growth of sales of a new advance and of deposit products. The volume of loans awarded in 2017-2019 increased by PLN 250 million, and the deposit balance by PLN 205 million.

Growing revenues and increased profitability of the project has been TMUB’s main goal since the beginning of collaboration with the mobile telecom.

An important part of development are changes in online and mobile banking which have been topped up with a number of functions, both transactional and handling-related, adapted to legal requirements.

In carrying out the digitisation project, the systems were expanded to include a number of selfservice functions, and the banking has been adapted to PSD2 Directive.

New functionalities and facilities for customers have been added in the transactional area as part of the development of the offering and the existing products, with a focus on making the payment products and mobile banking more attractive. In that development, the service of contactless payments by mobile phones has been expanded by including the functionality of adding virtual cards to GooglePay (Android) and ApplePay (iOS) directly from the Bank’s application level.

To ensure the highest possible satisfaction of customers with the entire digital banking, to enhance their comfort in using our systems and increase the transparency of information, a number of facilities for customers have been introduced, such as: the wire transfer form has been re-designed for operations involving currency conversion on the customer’s account, and in mobile banking the functions of retrieval of assessments and surveys of customer satisfaction have been introduced.

Alior Bank’s branch in Romania

Alior Bank’s branch in Romania

In 2019, Alior Bank’s foreign branch in Romania continued its commercial operations initiated on 18 October 2017 (operating activities began on 18 July 2016).

In 2019, the sales network for banking products was expanded both in outlet channels: 53 “SIS” (Shop in Shop) outlets, 129 direct sales agents, and 9 brokers, including the largest financial broker in the Romanian market – KIWI (figures as at 31/12/2019) and in remote channels: verification of customer identity has been enabled in the process of opening an account in digital channels using a “one-cent transfer charge”, and a functionality was implemented for acquiring leads for online advances, and collaboration has been started with 3 online financial intermediaries. This resulted in a dynamic growth of customer portfolio and increased share of new acquisitions of credit products in the market from 0.07% to 1.3%.

In 2019, work intensified related to the adaptation to the changing regulatory environment, resulting in the need to implement changes under new EU and national regulations on payments: PSD2 Directive and Cross-Border Payments Regulation; as well as the 4th Anti-Money Laundering Directive. The branch has continued servicing its customers in its own above-mentioned outlets (SIS) and in 240 points of sale (POS) of Telekom Romania, as well as through digital channels: website www.telekombanking.ro, mobile banking that provides for an innovative log-in and authorisation of transactions using biometric methods, and the updated version of the Currency Exchange Bureau platform https://schimb.telekombanking.ro/.

The plan for the subsequent months is to develop further direct sales channels and implement technical solutions to optimise sales of banking products, as well as innovative projects expanding the product range in digital channels, e.g.: the mobile app for the Currency Exchange Bureau platform. Further work will be focused on making available for new and existing customers of our Bank the possibility of applying for deposit and credit products completely online using the Bank’s mobile app. This project is being delivered in collaboration with FinTechs which use innovative, advanced solutions for the verification of identity and authentication of digital signatures. As at 31 December 2019, the Branch in Romania employed 243 full-time equivalents (115 FTEs at the Headquarters, and 128 FTEs at SISs).

Bancovo

In 2019, Bancovo intensified its marketing activities by launching its first TV campaign aimed at building brand awareness among customers. The marketing action has brought tangible effects:

In 2019, Bancovo intensified its marketing activities by launching its first TV campaign aimed at building brand awareness among customers. The marketing action has brought tangible effects:

- number of users increasing to almost 200,000 by the end of December 2019,

- selling more than 10,000 advances in 2019,

- six-fold improvement of operating performance of the project.

At the end of 2019, the company offered products of more than 25 financial institutions addressed to a broad range of audience, both to consumers (loans/advances), as well as to small-company owners (advances/microfactoring).

In 2019, there was not only swift development of the existing activities of the platform, but also introduction of new Bancovo business projects:

- in Q4 2019, the CASH platform – a joint venture of PZU, Alior Bank and Bancovo was launched in the market. Bancovo is a technology partner of the CASH platform which is the first in Poland to use the BaaS (Broker-as-a-Service) collaboration model. CASH implementation demonstrates that Bancovo’s solutions can be easily multiplied, the platform has an open IT architecture, which allows it to be promptly implemented in other business models in Poland as well as in other countries,

- in September 2019, Bancovo has expanded its loan brokerage offering to include hirepurchase financing by launching collaboration with the Polish biggest consumer electronics and home appliance retailer, EURO RTV AGD. Under that solution, Bancovo provides a loan engine and aggregates the offerings of selected financial institutions, which provides paperless financing for the goods offered by the retailer chain,

- In December 2019, Bancovo has launched a new lending process which uses the opportunities offered by PSD2 Directive, whereby customers can in an even more secure and friendly way obtain financing of their needs on the Platform.